It's the Econom(ies) Stupid!

Macroeconomics and Consumer Attitudes

This morning’s Denver Post included an Op-Ed from economist Paul Krugman that had recently appeared in the New York Times. Krugman starts his column with the well-known polling gaps between what people think about crime in general and how safe they feel in their own communities.

What does all this tell us, besides the fact that Americans are very confused about crime? It shows that on an important public issue, people can hold beliefs about what is happening to other people — people who live in other places, or in the nation as a whole — that are not just false but also at odds with their personal experience.

He wrote this piece as a follow up to one he wrote last week attempting to explore (as many others have been doing) why people feel so badly about the state of the economy. He rehearses all the important data points: the decline in the rate of inflation over the past year (although it ticked up slightly over the last two months according to this story by Rachel Siegel), consumer spending remaining strong, record low unemployment rates. So why are people so soured on the economy?

Jonathan V. Last made a similar (and wonderful) argument last month in The Bulwark. Where Krugman uses the crime data to make his point, JVL uses attitudes toward schools.

So let’s start with how people view America’s schools. Newsflash: Americans think our schools are terrible! Only 36 percent of Americans say they are satisfied with America’s K-12 schools.

There’s just one problem with that number . . .

76 percent of parents who have actual school-aged kids say they are satisfied with America’s schools.

In last week’s piece, Krugman argues (as do many others) about the role of partisanship in shaping attitudes toward the economy. Things are not objectively bad at the macroeconomic level but some feel like they are. And, of course, some are politically motivated to believe the worst about the economy under Biden and the best about the pre-Covid economy under Trump.

The bottom line is that there is a real disconnect between what Americans say about the economy and reality — not just official data, but even their own experiences. It’s silly to deny that this disconnect exists.

What explains negativity about a good economy? Partisanship is surely a factor: Republicans’ assessment of the current economy roughly matches what it was in June 1980, when unemployment was twice as high and inflation four times as high as they are now. Beyond that, the events of the past few years — not just inflation and higher interest rates but also the disruption Covid caused to everyone’s lives, and perhaps the sense that America is coming apart politically — may have engendered a sourness, an unwillingness to acknowledge good news even when it happens.

As many commentators have noticed, Republican memories of the robust economy in 2019 provides a bit of a mirage. You can’t just skip 2020 as if it never happened. And some key macroeconomic indicators are better today that they were in 2019: the Dow Jones1, Unemployment, New Hires, Wages.

But the other economy, the one where people live — I’m calling it the kitchen table economy — is slow to match these macroeconomic gains — even ignoring the potential partisan bias. I looked up the University of Michigan’s Consumer Sentiment Index to see how economic confidence was tracking. Here is the 50 year window.

For some reason, the baseline for consumer sentiment is set in 1966 terms (I was 12, so I don’t know why that’s the comparison). The vertical gray bars represent economic disruptions — Watergate, recessions, the financial crisis of 2007-9, Covid in 2020.

These patterns of consumer sentiment don’t necessarily align with the economics of a particular time period. The “stagflation” of the late Carter administration (high unemployment, high interest rates, high inflation) seem to bottom out it the upper 50s. The late 2022 trough bears nothing in common with that period. The 2008 trough of the Great Recession — which involved a threat to our entire financial system, massive home foreclosures, and high unemployment is somehow less bad that the Biden administration in 2022.

While the Infrastructure Act and the Inflation Reduction Act both have the potential to change these dynamics when their initiatives bear fruit (which probably won’t be until fall 2024 at the earliest), people see these as simply political talking points. It doesn’t help when Democrats cherry-pick a particular good thing in the legislation and make ads about how Republicans voted against it. It simply raises the salience of the political partisanship. Far better to talk about impacts over the next five to ten years.

In the Rachel Siegel story about the August inflation numbers linked above, we get the monthly factors pushing inflation up slightly.

Gas costs drove inflation in August, rising 10.6 percent over the month and accounting for more than half of the increase over July. All other major energy categories rose as well.

The shelter index, which is largely made up of rent costs, rose for the 40th consecutive month. Rent rose 0.5 percent in August, slightly hotter than the 0.4 percent notched in July.

There were a few exceptions: Costs for used cars and trucks eased 1.2 percent last month. But the scant signs of progress were dwarfed by other measures. Food costs rose 0.2 in August, the same rate as July. Prices for car insurance rose 2.4 percent, and medical care rose 0.2 percent after falling in July. Airfares also reversed course, climbing 4.9 percent after multiple months of cooling prices.

I’m always fascinated with how these factors operate on the ground in the kitchen table economy. Increases in housing costs are felt only when a renter renews a lease, not month to month. Car prices and insurance are similarly periodic expenses, felt when one buys a new/used car or when the policy renews. Airfare is up but most people are infrequent travelers.

That leaves gasoline and food. Those are the big drivers of actual household budget crises. There are two points to consider here. First, gas prices are driven by global issues of supply lines and weather disruptions. They will rise as Saudi Arabia reduces production in spite of the rise of domestic energy production in the US.2 There is little that any administration can do to make much of an impact on them.3

Food costs are similarly a function of externalities. Weather disruptions, corporate consolidation, disease (bird flu) can all serious disrupt normal supplies.

So the response to the claim that things are getting better is always, “Really, have you put gas in your car? Have you bought eggs lately?”

But here’s the thing: Prices Are Not Going Down!

Sure, when the supply disruption passes, there will be an easing of prices. But I guarantee that those new prices will still be slightly higher than they were before the disruption occurred. A new baseline will be set against which we’ll compare tomorrow’s prices.4

Don’t blame Biden. Blame Capitalism.

Those prices will inch up. Consumer purchasing will inch up to take that into account.5 I now spend almost $6 a box for my supply of Family Size Frosted Cheerios. I’m likely to continue to buy my Cheerios as opposed to whatever store brand is available (but I did take big advantage of a sale this week and scored several boxes at $3.50 each).

There’s another implication to the U of M consumer sentiment chart. We can think of those major dips in confidence as societal disruptions. In 1974, 1979, 2008, and 2002 there is a sense in which society simply isn’t working as it’s supposed to. Even as things get better at the macroeconomic level, there is a fear that maybe things are so broken that we have no continuity with the before times.6

Of course, in the midst of the pandemic we put money into family budgets. This was important in maintaining stability during the disruption. But the money that provided such a cushion is now pretty much spent. In addition, the expanded Child Tax Credit expired at the end of 2022, which has resulted in a dramatic increase in child poverty which reversed the earlier impact it had.

It’s likely true that the stimulus money made the inflation crisis worse. From a macroeconomic perspective, one could argue that it was a mistake. But from a kitchen table economic perspective, it was essential. Could it have been more narrowly targeted? Of course. But the lesson from 2008 is that waiting to act or acting cautiously makes the long-term recovery harder for those families who need help.

One thing that would help consumer attitudes about the economy would be for all stories about macroeconomics to remind people of what normal pricing looks like. I don’t think I’m a rabid Anti-Trumper (okay, I am) in pointing out that prices of housing and food and gas increased between January 20, 2017 and January 20, 2021. Stories about individuals buying gas for their monster truck or buying 9 gallons of milk for their very large family are not at all helpful because they use abnormal anecdotes to color in economic trends.

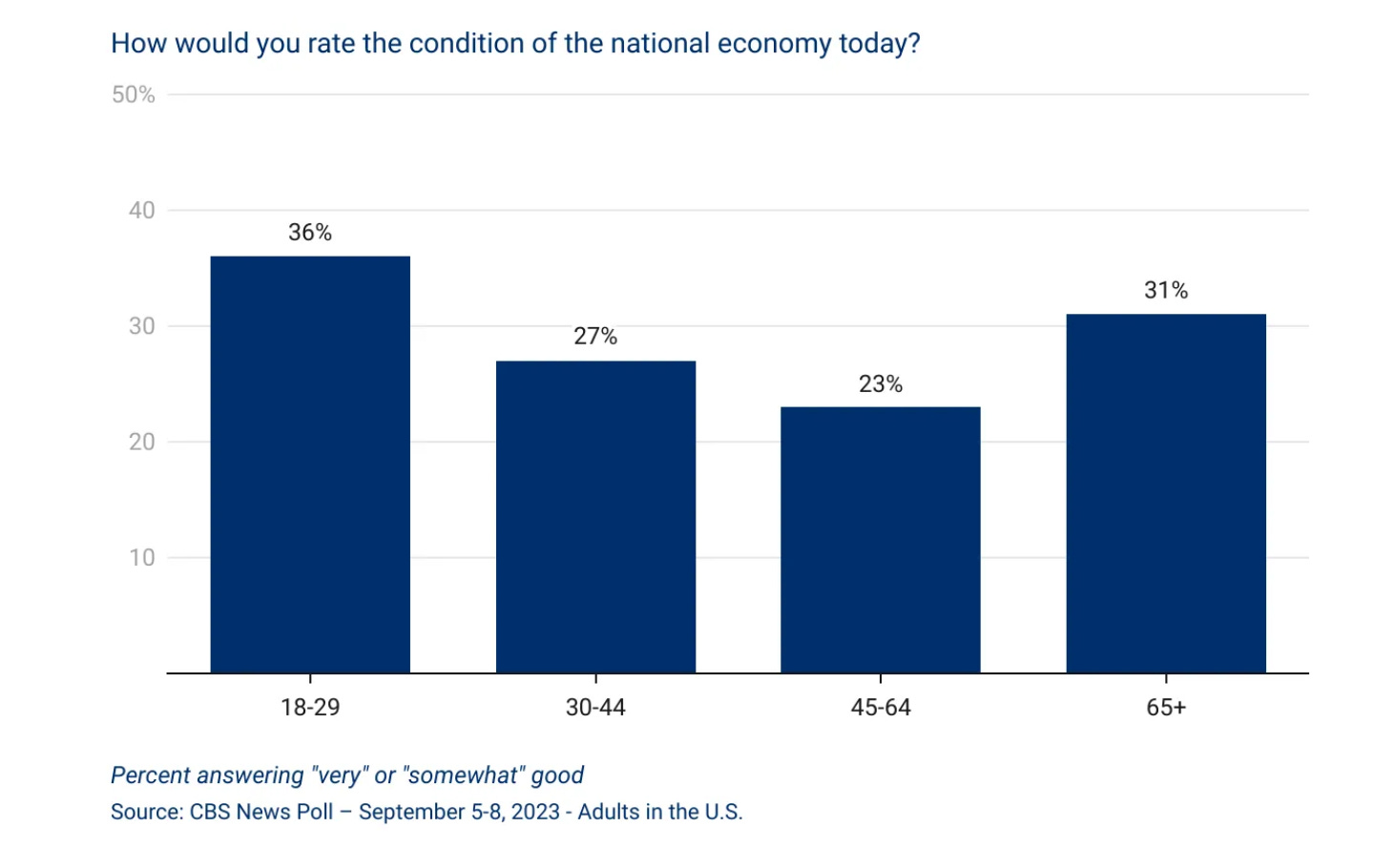

Not all is terrible in attitudes surrounding the kitchen table economy. I’ve recently started following John Della Volpe’s Substack (highly recommended). His is doing remarkable research on the younger generations. I learned in a Brookings Seminar yesterday that those under 40 will make up 50% of the voting public in 2024. This week John shared some new data on young people, including their attitudes toward the economy.

I think this data is similar to the argument I’m advancing here. The young people under 30 have little experience with the Before Times. They have seen multiple disruptions in society over the last decade or so. But they are remarkably resilient and surprisingly optimistic about their future.7 And of course, they don’t watch cable news (especially Fox News) or read major newspapers, instead8 getting their information from friends and YouTube.

Watch these folks. They are going to be key to what happens in 2024 and the next decade beyond.

I’ll never forget our TIAA advisor telling us in 2019 that the market, then at 25K, was due for a reset and we should be prepared. As I write this, the Dow is at 34,600.

Which is higher than it’s ever been.

And, it has to be said, every time the media decides to talk about gas prices with a screen shot from a gas station in Los Angeles or tell a story about the guy who is outraged at how much it costs him to put 30 gallons into his mammoth Ford 250.

A favorite conservative talking point is to look at gas prices in the midst of the pandemic when the lack of demand due to everyone staying home caused them to bottom out.

New reports will talk about how people are frustrated with the increased costs of travel and hotels for vacations but will rarely point out that people are, in fact, taking vacations.

One of the first sociology lectures I developed was based on Kai Erikson’s treatment of the 1972 Buffalo Creek flood in West Virginia. A mining dam broke and flooded the entire community. Even after the cleanup, people remained suspicious of nature and their neighbors, believing that another disaster might be just around the corner.

I probably could have looked into the crosstabs to see what percentage said “terrible”.